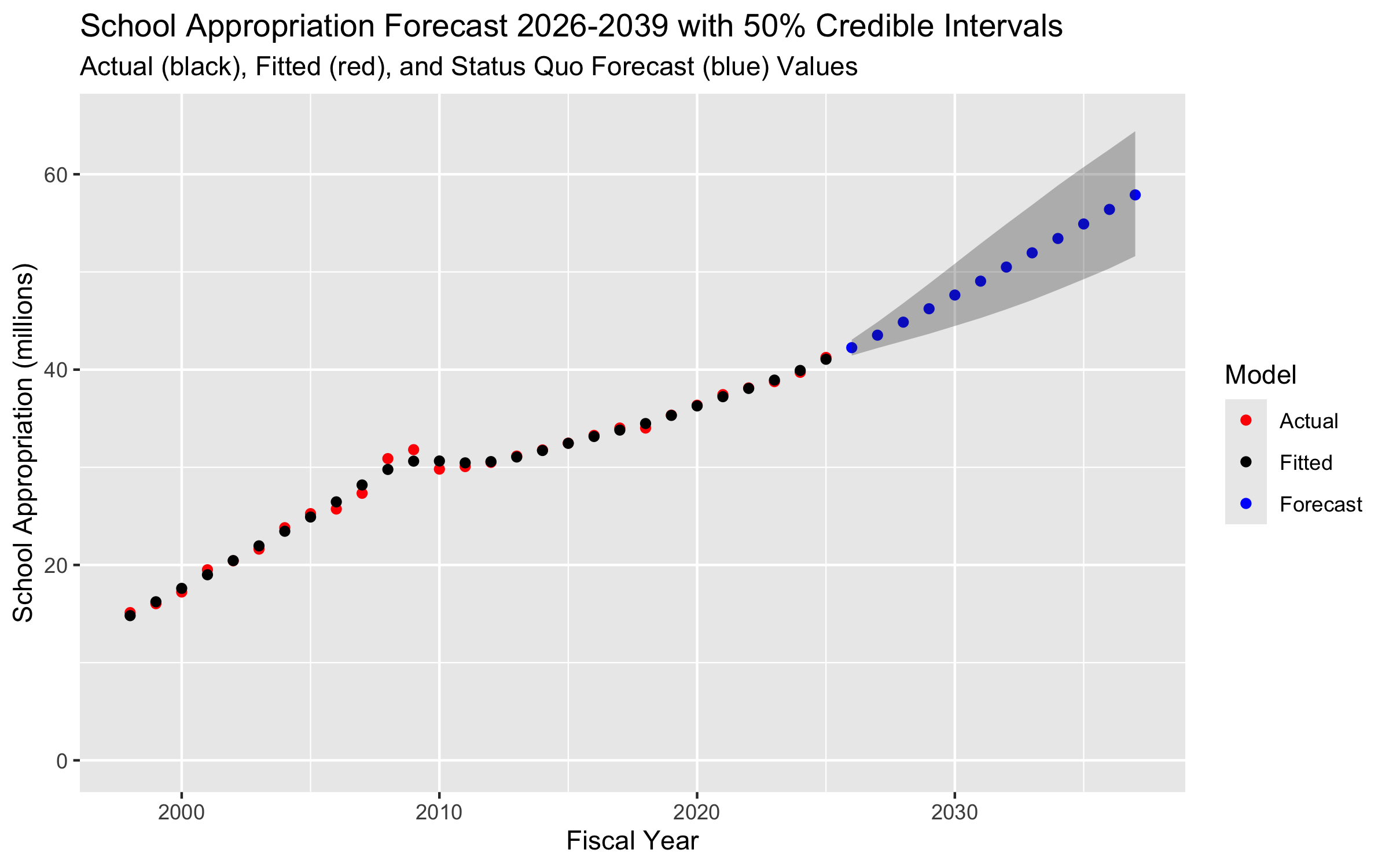

School Appropriation 1998-2025 with Timeseries Forecast through 2039.

- This is a timeseries version of a forecast model presented at the last meeting.

- Timeseries models are standard tools in financial forecasting.

- They have been around for many years in the form of ARIMA (Autoregressive Integrated Moving Average) or classical time series models.

- A Gaussian Process model is often the timeseries of choice for 21st century forecasting.

- With timeseries, the number of parameters does not increase with the number of years ahead to forecast. This is a significant advantage over projection methods and makes longer term forecasts possible.

- Another advantage of timeseries models is that you can validate them by turning the clock back and forecasting years you already know the result for.